Jan Dhan: Narendra Modi's Speed Problem

(Mumbai autorickshaw driver Arjun Dubey has applied for a bank account under the Prime Minister's Jan Dhan Yojana. He said he opened the account only to receive government subsidies.)

MUMBAI: Hanumant Vithoba's vision was dimmed by cement dust blowing into his eyes and his back was bent from hauling cement sacks into trucks. Vithoba, 92, worked for ten years in a cement factory in Sewri, a grimy, polluted port district on Mumbai's eastern seaboard. After ill-health finally forced out of his job, Vithoba, the only wage earner in his family, retired to a shack. He had no savings and no hope of correcting his dimming sight.

Last week, new information and hope suddenly reached Vithoba. He hobbled over to a local temple and joined many others in opening a bank account under the Pradhan Mantri Jan Dhan Yojana (PJMDY), the Prime Minister's People's Wealth Programme. This is the much-publicised game-changer that Narendra Modi extols, a move to bring banking services to India's vast unbanked population, to slash runaway corruption in government spending and allow social-security payments to directly reach millions of poor people.

But Vithoba's hopes are a warning to the hurdles facing Modi's ambitions.

Asked what he expects from his new account, Vithoba replied: "I have heard that the government will give us money if we fall sick, if we need to pay for our treatment at the hospital, or if we meet with an accident. I will use that money to operate on my eyes."

Clearly, Vithoba's expectations are misplaced. As IndiaSpend's interviews at PJMDY account-opening camps in the poorest areas of India's financial capital revealed, he is not the only one.

Sultana Shah, a mother of two and resident of a slum in the central Mumbai suburb of Ghatkopar, was clear why she needed a PJMDY account. “My husband is a peon who makes barely Rs. 5,000 a month and I have two children," she explained. "It's difficult to make ends meet most times, and this money will help keep us afloat."

Across town, in his office, Assistant General Manager of state-owned Punjab National Bank (PNB), Om Prasad is visibly upbeat at the speed with which new accounts are being opened. "Our target for the inaugural day was 250 accounts per branch, and we far exceeded it, across branches."

PNB opened roughly 1.8 million accounts nationwide on August 28, part of the 15 million opened that day, as Modi kicked off what is touted as one of the world's greatest banking revolutions.

"I wish to connect the poorest citizens of the country with the facility of bank accounts,” said Modi. “There are millions of families who have mobile phones, but no bank accounts. We have to change this. The change will commence from this point... Never before in economic history have 15 million bank accounts been opened in a single day. Never before have insurance companies issued 15 million accident policies in a single day. Never before has the government of India organized a program of such scale — over 77,000 locations — with the participation of so many chief ministers, union ministers, and government and bank officials”

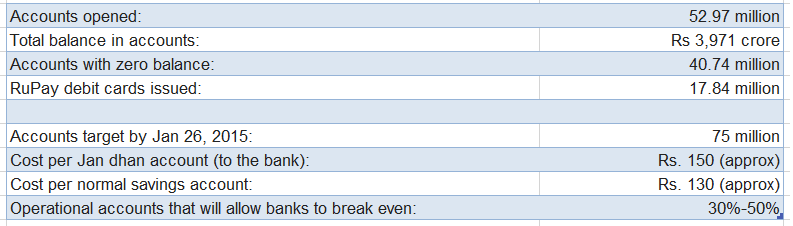

Speed Money: Prime Minister's People's Wealth Programme (Jan Dhan Yojana)

(Sources: Department of Financial Services, Ministry of Finance; Axis Bank, Punjab National Bank; all figures as on September 29, 2014)

Although not at this pace and scale, India has seen a previous attempt at revolutionising grassroots banking.

In the five years to 2010, the previous United Progressive Alliance (UPA) government opened 50.6 million no-frills accounts--the PJMDY reached 52 million accounts in just two months--meant primarily to directly deliver payments for various social-security programmes, from old-age pensions to jobs-for-work programmes. To bypass the lack of bank branches, business correspondents were used--agencies that opened accounts and handed over payments to accounts holders.

The First Time: No-frills accounts opened by previous government

Accounts opened: 50.6 million (between 2005 and 2010)

(Rajasthan's high utilisation of bank accounts is attributed to the wide spread of social-security programmes, particularly the jobs-for-work, MNREGA scheme)

Three independent studies (CMF, MicroSave, Skoch) have previously shown that up to 90% of these accounts are inactive.

Reserve Bank of India Governor Raghuram Rajan has cautioned banks about the risks of focussing on numbers alone in the PJMDY plan.

At a recent banking conference, Rajan said: “When we roll out the scheme, we have to make sure it does not go off the track. The target is universality, not just speed and numbers. The system is going to be a waste if what we do generates a whole set of duplicate accounts."

There are already indications that duplicate accounts are being opened. Banks have no way of knowing if someone opening a Jan Dhan account already has an account. This account is from banking columnist Tamal Bandopadhyay:

"I happened to be present at minority affairs minister Najma Heptulla's launch function in Kolkata. Forty-odd financially included persons, who opened accounts on that day, walked into a five-star hotel for the first time in their lives and were treated to tea and cookies after Heptulla handed over to them a RuPay debit card and a passbook...It didn't take much time to find out that for all of them, it was not their first bank account. Clearly, the banks wanted to meet the target at any cost."

Rajan said that the focus of account openings must not be only on opening them.

"It is going to be a waste if you do not have full coverage," he said. "It is going to be a waste if those accounts are not used, they open and they languish. Many of the persons who are coming into the system are coming for the first time, so if we don't make a good first impression, they will stay out."

No frills for customer, no money for banks

Kirandevi Ramkumar Gupta, 36, does not have a good first impression about basic banking.

She and her husband, an auto driver, opened a no-frills account--to do away with the stigma attached to the term, the RBI in 2012 changed its name to Basic Savings Bank Deposit Account--with the Bank of Baroda one-and-a-half years ago, so that they could receive cooking-gas subsidies.

The couple only ever received one subsidy of Rs 600.

"After that we have not used it," said Gupta of Kamraj Nagar, a slum of untidy concrete homes in central Mumbai.

PNB's Prasad acknowledges the failure of no-frills accounts. He cites the example of Sakherseth town in Maharashtra's Thane district where only a little over 20% of 9,000 No-Frills Accounts and Basic Savings Bank Deposit Account accounts opened more than two years ago are active.

Most of these accounts were opened for Mahatma Gandhi Rural Employment Guarantee Act (MNREGA) payments, but of the 2,000 active accounts only 600 received any payments. “The accounts that have received any payment have seen a 100% withdrawal rate; and the 1,400 accounts that are still active have almost no balance in them,” said Prasad.

PJMDY accounts and those that preceded them cost banks upto 15% more than normal savings accounts. This is because of the extra staff required, travel and camp-site expenses, printing and other expenses to drive awareness, various bank officals told Indiaspend.

“The process cost—forms, debit card, documents verification procedure—is the same (as normal savings-bank accounts),” said an Axis Bank official, requesting anonymity, since he is not authorised to speak with the media.

At Axis Bank, one of India's largest private banks, opening a PMJDY bank account costs approximately Rs. 100. The bank has 2,500 branches and expects to open about 1 million accounts byJanuary 26, 2015. For the bank to break-even, it needs at least 30% of them to be active.

Banks were clearly unenthusiastic about no-frills accounts, and it appears apparent that growth did not translate to financial inclusion.

The number of branches of Scheduled Commercial Banks in India increased manifold from 68,681 in March 2006 to 1,02,343 in March 2013; and the number of BSBD accounts opened increased from 73.45 million in March 2010 to 182.06 million in March 2013.

As this 2011 study said: "Banks are not allowed to charge the customer for the No-Frill Accounts, and find them intrinsically loss-making. Thus, banks are doing little to market their benefits or encourage their use. This has led to extremely high levels of inactivity in the No-Frill Accounts...underlining that the objective of financial inclusion has not really been met."

The hardest part: Getting subsidies into bank accounts

While most people opening basic bank accounts do it for the subsidies and government payments, many beneficiaries just don't receive them.

The World Bank estimates that only 4% of India's adult population use its accounts to receive government payments, which run into billions of dollars, a vast percentage of which is siphoned off by corrupt officials or through other leaks.

According to a paper by the National Institute of Public Finance and Policy, a New Delhi based public economics and policy research institute, subsidy payouts by the government for the year 2010-2011 stack up thus: total food subsidy Rs. 58,500 crore, wage expenditure bill MNREGA, Rs. 24,864, and fertiliser subsidy, Rs. 62,301 crore. The total LPG subsidy was Rs. 23,746 crore, and national education subsidy, Rs.31,036 crore. There are many other subsidies, including those for pensions, housing, scholarships, childcare and toilets.

If subsidies to millions of beneficiaries could be paid directly into their bank accounts, using Aadhaar, or the Unique Identity scheme, the savings to the government would be Rs 20,265 crore, said the NIPFP estimate.

More than 680 million Indians have been legally identified and a unique number allotted to them. The government has now given the Unique Identification Authority of India (UIDAI) a target of 1 billion enrollments by 2015. This exercise will apparently run parallel to the spread of banking, seeking to provide banking services to about 600 million who cannot presently access them.

These are impressive numbers and herald ambitions with few global precedents, although they build directly on the experiments and programmes begun by the UPA.

Indeed, the very scale of the banking programme--and the speed asked of it--is cause for worry.

Yet, there is little doubt that India needs a massive banking expansion for its poor, but gradually prospering population.

Among the currently excluded population, there are two broad sub-categories, Managing Director and CEO of Yes Bank, Rana Kapoor, told Knowledge@Wharton, an online journal of the Wharton Business School. “There is [the] segment that has both need of financial services and the inclination to pay reasonable charges for them. The rapid proliferation of microfinance institutions and gold loan non-banking finance companies highlights this potential. The other segment is that of people heavily dependent on state subsidies for their livelihood. For this segment, though the other financial services may not be relevant, having a savings account to receive these subsidies without pilferage is highly desirable.”

According to data from the Global Financial Inclusion (Global Findex) database, only 35% of the population above 15 years of age has a bank account at a formal financial institution—a bank, credit union, cooperative, post office, or microfinance institution. This is significantly lower than other the BRICS economies of Brazil, Russia, China, South Africa where the average is 61%.

Another issue that has plagued financial inclusion in India is that a large number of banking correspondent agents, the route that many banks use to reach the unbanked, are only in bank records. In a survey of 2,932 villages with a population of greater than 1,000, only 39% were covered through customer service points (CSPs), according to this 2012 report. Only about 6.6% of villages had “transaction ready” CSPs against the reported achievement of one CSP in every village with a population over 1,000.

The result is that even in cities, there are many who are untouched by formal banking.

In a slum in the tony western Mumbai suburb of Bandra, auto driver Sheikh Mehamood, 41, does not know that money saved in a bank can fetch him interest. He never had money to save and never opened a bank account because "banks always ask for so many documents and a minimum balance of Rs 1,000".

Mehamood is, however, aware that a bank account can benefit him. "For a person who does not have anything, whatever extra they get is good for them."

Jan Dhan: What's different this time?

"In a word, implementation."

That is the assessment of a bank CEO, speaking on condition of anonymity, about the difference between the UPA's no-frills accounts and the PMJDY. He describes continuous, subtle and not-so-subtle, pressure from the Prime Minister's Office and the Finance Ministry, ever since Modi launched the programme. Targets are set, revised and closely monitored.

“This programme itself is not very different from what we had earlier. But, the execution is much much better. Earlier we concentrated on villages. Today we are looking at a conglomeration of families—every household should have an account. Banks have to conduct surveys in the allotted areas on how many households don't have an account and then subsequently open them,” the Axis Bank official said

“The real difference between this programme and the others is that it is being monitored,” he said. “We have found that if people are being watched they behave better.”

Aside from the scale, speed and close monitoring, the PMJDY hopes to be more than a vessel for subsidy payments. The plan envisages at least one basic banking account to each household, a RuPay debit card with an in-built insurance cover of Rs 1 lakh, an overdraft facility of Rs 5,000, if the account is operated satisfactorily for six months, and a life-insurance policy of Rs 30,000 for acounts opened before January 26, 2015.

The CEO likens the megascale approach to a hosepipe. "Open the spigot so wide that a lot of water will be wasted, but there will be so much water that the plants will get watered."

M.S. Sriram, a professor at the Centre for Public Policy at the Indian Institute for Management, Bangalore, is sceptical of such an approach. “The current methodology serves political interests—it can claim and count numbers and tout achievements," said Sriram. " There is no meaning in these achievements unless we see at least 10-15 transactions in a year in these accounts.”

Financial inclusion programmes are likely to be successful only when the accounts have transactions not just be a vessel for handouts and subsidies, he said.

(A camp conducted by Karur Vyasa Bank, in Kamraj Nagar, a slum in Mumbai's eastern Ghatkopar suburb, to open bank accounts under the Jan Dhan Yojana.)

“Whenever there has been transaction-led initiatives (providing loans under the old schemes, having savings and credit under the self-help group movement) they have worked, but just opening accounts is tokenism. What is the use of opening accounts and touting the numbers if nobody is using them?”

The UIDAI's effort have been mammoth and unprecedented. But, for a more efficient Direct Benefits Transfer system (as cash transfers are called in India) to be put in place, Aadhaar seeding must become more extensive.

“Bank accounts can be really effective if Aadhaar seeding is done properly. Once that happens government benefits will automatically go to the Aadhaar-linked account and people will have an incentive to be within the formal financial system,” said the Axis Bank executive.

“The Swaabhimaan (no-frills accounts) programme of UPA and the PMJDY of the NDA (National Democratic Alliance) are interesting programmes, but I believe they have got the sequence wrong," said IIM's Sriram. "We first need to create a system that demands accounts--by ensuring that people see the benefit in opening an account--not by offering baits like insurance, but by making transactions easier.”

While the UPA government started well by mandating that MGNREGA payments and other benefits be paid through a bank account, they faltered by having a business-correspondent model that kept customers away from the banks.

“How would they (customers) deepen their financial transactions with the banking system if they are always dealing with the BC, who only makes payments?" said Sriram. "If they have to discover the range of the banking facilities that they could use, they need to be familiar with the bank."

Indians seek that familiarity. A November 2013 RBI survey reported that in a sample of 34,149 people in rural India, 76% were aware of services offered by banks: "The study shows that there is financial awareness and demand for banking services in rural areas. Hence, if access can be provided, usage of banking services will improve. Major factors hindering access are the non-availability of banking outlets and long distance of existing banking outlets."

These stumbling blocks have not been addressed, and so the warnings of RBI governor Rajan and other experts. Politically, the misplaced expectations of those like Vithoba and Shah could snowball into disillusionment, as India's previous government experienced.

It does appear clear that India will have the 75 million bank accounts the Prime Minister seeks by Republic Day, 2015. It is the only thing that is clear.

Photographs: Arlene Chang; Vizualisation: Sanjit Oberai