India's 10,000 Farmers-Collective Plan Needs Funds, Professional Management

Bengaluru: India’s plan to collectivise and support millions of small and marginal farmers into profitable business groups may fail without significant reforms in the existing funding and support ecosystem for farm collectives, experts say. In five years to 2023-24, the government plans to set up and support 10,000 new Farmer Producer Organisations (FPOs), where farmers come together as shareholders to expand the production and marketing of their agricultural output.

Apart from shareholder funds and bank credit, these groups also receive some initial financial support from government agencies.

Upto 86% of landholdings in India are small and marginal, with low outputs and paltry incomes--the average monthly income per agricultural household was estimated to be Rs 6,426 in 2014. Many farmers’ groups are struggling to survive or expand because small farmers find it hard to pool in enough money as shareholders and banks do not find them creditworthy enough to give them loans, we found. The low availability of funds also does not permit collectives to employ professional managers with business skills.

Under the new FPO guidelines, the government will provide financial support of upto Rs 18 lakh to new organisations for the first three years. But new FPOs need support for at least five to seven years to grow and stabilise, and existing cooperatives must get better access to bank credit at low rates in order to compete with rich private companies, said experts.

Take the example of Devnadi Valley Agricultural Producer Company, a Nashik-based farmer producer company (FPC), included in the broader category of FPOs under part IX A of Companies Act. It was set up in 2011 and in the nine years of its existence, the company has seen three profitable years--all in the last five years. Its membership has grown 34 times to 850, comprising mostly small and marginal vegetable farmers.

However, the company is still struggling to build and expand into a viable business because of inadequate financial support from the government, said farmer and managing director Anil Shinde. Devnadi’s infrastructure for packaging and storing its products--mostly onions, tomatoes and other vegetables--is still not good enough to ensure efficient delivery.

Devnadi’s problems--access to government funds, problems with raising bank loans to be able to compete with big traders in mandis and rich private players--reflect the hurdles most existing farm collectives face and new ones are likely to run into.

An FPO can grow as an institution that helps mitigate farm risks only if the government makes timely and sufficient investments over time, said C. Shambu Prasad, professor, Strategic Management & Social Sciences at Institute of Rural Management, Anand (IRMA). “A good FPO cannot be formed in less than five years based on our experience,” he said.

Cooperatives have existed in India over a century; dairy collective Amul in Gujarat is one of the best-known and successful of these. But over time, these groups became dependent on government funds and thus prone to bureaucratic and political interference. To address these issues, the Y.K. Alagh Committee (2000) recommended the creation and introduction of producer companies that allow the cooperative spirit to co-exist with the operational flexibility of corporates. Over the years, various state and national initiatives have helped form FPOs and producer companies.

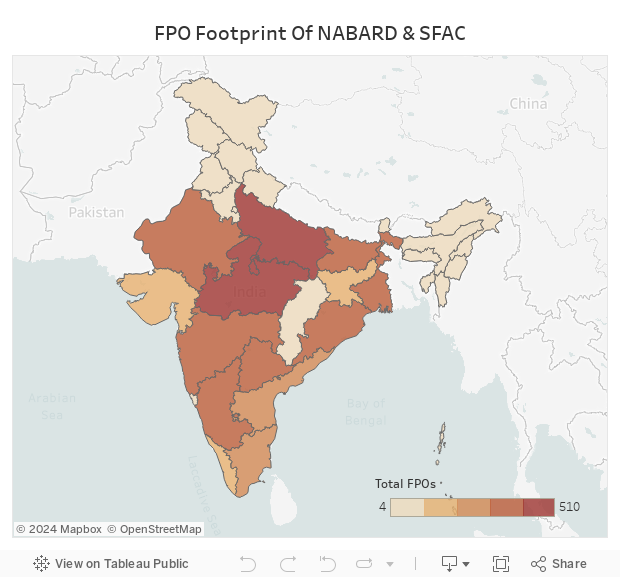

There are no consolidated data on how many such groups already exist in India but there are two available estimates--4,235 supported by the National Bank for Agriculture and Rural Development (NABARD) and 876 by the Small Farmers’ Agri Business Consortium (SFAC) promoted by the Ministry of Agriculture, Cooperation and Farmers’ Welfare.

The ruling Bharatiya Janata Party-led government has promised to double farm incomes by 2022--the average monthly income per agricultural household, as we said, was estimated to be Rs 6,426, according to 2014 government data. But there have been several protests against the new farm laws aimed at achieving this target.

No consolidated figures for farm collectives

Seven months after the July 2019 budget, when the Centre announced its intent to form 10,000 new FPOs, a government order approved a dedicated central sector scheme for their promotion and support and allocated a budgetary support of Rs 4,496 crore ($607 million) until 2023-24. New operational guidelines for promoting and supporting 10,000 new FPOs were released in July.

As of now, there is no consolidated database on FPOs, so the Centre does not know how many exist already. They were formed mostly with the support of different government agricultural bodies such as NABARD and SFAC, both of which maintain different databases. This makes it difficult to design or implement any interventions or create regulatory mechanisms to promote the growth of FPOs.

A March 2020 report, Farmer Producer Companies: Past, Present and Future, by Azim Premji University scholars showed that 7,374 producer companies had been registered with the Ministry of Corporate Affairs until March 31, 2019, but this was twice all previously published estimates. This confusion over numbers is a “concern, as there is a renewed thrust to start more FPOs”, said a December 2019 report by Shambu Prasad of IRMA. Reliable data are a must for policy design and implementation, and for regulation of different categories of FPOs.

The NABARD database consists of only FPOs registered 2014 onward after it launched a fund for the support and promotion of FPOs--the Producers’ Organization Development and Upliftment Corpus (PRODUCE). But there are no figures available from before 2010, the IRMA report noted.

Source: Small Farmers’ Agri Business Consortium (data as on October 31 , 2020) and National Bank for Agriculture and Rural Development (data as on August 15, 2019)

Note: Data for Jammu and Kashmir are for the erstwhile state, including for the union territory of Ladakh

To rectify this, the new guidelines have suggested a National Project Management Agency (NPMA) to function as a national-level data repository which will maintain an integrated portal for FPOs. In addition to data-related requirements, it is expected to function as a digital platform for maintaining records on membership, activities, business growth and annual accounts of FPOs.

Poor government support, few shareholder resources

FPOs are expected to run like businesses though they are formed by small and marginal farmers with few resources and little business acumen.

Farm cooperatives have a problem mobilising funds on two fronts--one, creating sufficient paid-up capital from shareholders; and two, obtaining credit from banks to sustain daily operations. Banks do not see small farmers as creditworthy because of previous unpaid loans and their lack of capacity to develop business plans, as we explain in the next section.

As for the shareholders, it is unrealistic to expect poorer farmers to contribute large share capital, pointed out Annapurna Neti, a co-author of Azim Premji University’s report. “If the intention is to increase farm incomes, we need to enable FPCs to operate well as their [primary] aim is to provide better incomes to a vulnerable population for whom farming is their primary livelihood,” she said.

An early-stage FPO will need to mobilise a minimum capital of Rs 3-5 lakh from shareholders to take up business activities and investments worth Rs 15-20 lakh to begin operations, estimated Nabkisan, a NABARD subsidiary for promotion and expansion of agricultural and allied enterprises.

Devnadi, for example, has raised Rs 8.5 lakh as paid-up capital from its shareholders by selling shares at Rs 1,000 per unit. In India, 86.4% farmer producer companies are like Devnadi--they have less than Rs 10 lakh as paid-up capital, as per the Azim Premji university report. Half of them have a paid-up capital of under Rs 1.1 lakh.

Just 20 FPCs--mostly working in dairy and plantation--have raised 60% of the total paid-up capital of Rs 844 crore raised by India’s 6,926 active farm companies, the report said. This indicates the inequalities in Indian agriculture where older sectors such as dairy and plantation do much better than new companies in other sectors.

In 2014-15, NABARD introduced PRODUCE, a fund that offered every FPO Rs 9 lakh over three years to help them become self-sustaining. This is not enough, said Prasad, because early stage FPOs need funds for multiple reasons--to run daily operations, pay employees and other liabilities. The World Bank’s District Poverty Initiatives Project, a rural poverty alleviation programme, gave Rs 25 lakh to new FPOs with a provision of working capital, he pointed out.

There are additional funds available from organisations like NABARD for FPOs that can meet certain milestones such as a high turnover target or increased membership. But given their limited ability to expand, most FPOs may not meet these targets, said Hiren Borkhatariya, manager, FPO facilitation centre, Yuva Mitra, a resource support agency for NABARD in Maharashtra.

Why new fund infusion may not be enough

Under the new FPO guidelines, the government will provide financial support of upto Rs 18 lakh to new organisations in their first three years, as we said. This support, which will not include management costs, will last till 2027-28 with the addition of Rs 2,370 crore to the government’s FPO kitty. In all, the government’s total budget to support FPOs upto 2027-28 will be Rs 6,866 crore ($927 million).

This support is expected to make FPOs “sustainable and economically viable”, as per the new guideline. From the fourth year onwards, FPOs are expected to manage without this assistance.

Earlier, there were no specific or separate schemes to promote and support FPOs, but the new policy guideline has changed that, said Neelkamal Darbari, managing director of SFAC. In terms of funding support from the SFAC, “the new scheme envisages increase in support [from SFAC] from Rs 1,000 per shareholder to Rs 2,000 [equity grant] and membership [requirement] of FPO has been decreased from 1,000 to 300 farmers”.

Although the government has increased hand-holding and financial support for new FPOs based on its own experience and the feedback from companies, this may be inadequate, said experts. For example, the government is still silent on the need for working capital in the short term.

Some of the guidelines, such as those on the release of funds on the basis of the execution of business plans, are “unrealistic”, said Prasad. “In agriculture this is difficult, and sticking to a business plan for five years is unrealistic,” he said. “This is counter to learning from the startup culture that appreciates the need to iterate while running an enterprise.”

Although the new Farmers’ Produce Trade and Commerce (Promotion and Facilitation) Bill, 2020 has little to say about FPOs, it has allowed farmers to sell outside the mandi or agri market yard which are influenced by middlemen, powerful traders, and commission agents.

But the relationship between the trader and farmer goes beyond transactions. “The trader provides inputs and buys produce at the farm gate,” said Neti of Azim Premji University. “There are a range of services which an FPC needs to offer to compete with the trader.”

Farmers like Rajesh Krishnan who heads the Thirunelly Agri Producer Company (TAPCO), an FPC, feel that the new farm laws will not support farmer collectives as they do not help create support structures. Through the new farm bills, “it looks like the government wants FPOs to support structures and supply-chain for big private players,” he alleged.

Bank loans hard to come by

For producer companies with existing loans and no collateral, it is difficult to raise credit from banks. “Our fund requirement depends on demand and production,” said Shinde of Devnadi. “Farmers need immediate cash payments. Often it takes five or six days to receive the amount [from customers]. We sometimes give a post-dated cheque if payment cannot be made right away to convince farmers.”

Banks are not accustomed to dealing with entities like FPOs--they are mostly used to giving loans to individual farmers. Further, banks are unsure of the creditworthiness of FPOs due to issues of debt and loan repayment among farmers and their low initial capital, as we said. With few business skills, FPOs cannot create the kind of robust business plans that impress banks.

Take the example of the one of the more successful FPOs, TAPCO that buys special traditional varieties of paddy. On a seasonal basis, the company needs upto Rs 40 lakh for procurement from almost 200 farmers. In 2020, this amount is expected to go up by another Rs 15-20 lakh because the company is expecting an increase in the number of farmers and their yield, Krishnan estimated.

But TAPCO’s Krishnan complained that banks are charging his company “unfair” market rates on loans--10.5%--while individual farmers are given loans at subsidised rates.

“Banks are quite happy giving us loans now as we have not been defaulting on repayments,” said Krishnan. But the problem is that the repayments will end up eating into the company’s turnover and profit, he added.

Devnadi reported a similar problem of having to pay a market interest on loans. The company is required by an organisation like SFAC to maintain a certain amount of produce as stock (like fertilisers, seeds, etc.) to renew its credit guarantee fund. To ensure that stocks are maintained, the company needs regular fund flows but the banks’ 12% interest on loans has to be paid even in bad years, said Shinde.

Other farm business groups may not be as lucky especially if they are dealing with goods that are listed under government procurement prices or the minimum support price. This pricing system is vulnerable to distortion because it may be set high despite low demand or end up depressed due to the release of old stock, estimated G.V. Ramanjaneyulu, executive director, Centre for Sustainable Agriculture, a resource organisation that supports training of FPOs formed by NABARD in Andhra Pradesh and Telangana. This distortion does not allow small farmers’ groups to get remunerative prices, reducing their ability to compete with mandis and big players.

Management skills wanted

With poor fund availability, FPOs are unable to attract employees with the kind of business acumen that farmers’ collectives lack. For example, NABARD provides Rs 9 lakh over three years and of this amount, the FPO receives Rs 5 lakh and the promoting organisations such as NGOs, Rs 4 lakh. With this kind of funding it is hard to offer attractive salary packages, said Krishnan.

In the case of TAPCO, there are three employees including Krishnan, and they cannot be shareholders as per the law. “We have kept our salaries low so that we can be viable. The CEO receives Rs 15,000 per month at par with wage labour. We want to improve staff salaries once business improves,” he said.

As companies, FPCs are obliged to file tax returns and comply with related laws as large corporations do. This needs understanding of legal and compliance-related complexities. Also, while farmers are exempt from income tax, registered companies are not. This makes it essential for FPOs to find qualified employees who understand the nuances of building a business.

Although the government announced a five-year tax holiday for FPOs with turnover of upto Rs 100 crore in the 2018 budget, they are not exempt from paying Minimum Alternate Tax (MAT), a provision to limit tax exemptions for companies. “We are taking up with the government on providing by working on exemption for MAT,” said G.R. Chintala, chairperson, NABARD.

Way forward: Invest in existing FPOs

IndiaSpend spoke to experts and members of existing farm business groups and collated suggestions on how FPOs can be supported better.

- Invest in existing FPOs and institutional structures that have evolved over decades. All three implementing agencies--SFAC, NABARD, National Cooperative Development Corporation--need to develop policy by regularly engaging with the FPOs.

- Invest in resource institutions and promotional organisations. Create steering committees on FPO support and formation at district and state levels that include organisations with FPO experience.

- Create state-level consortiums to design FPO policies because the state is a vital unit in the agricultural sector. Federated models like Amul, not individual FPOs, can be considered for this.

- Create incubation systems for new FPOs and help them integrate government support services.

- Facilitate onboarding of business expertise and promote agencies based on the maturity of FPOs considering they may need five to seven years to stabilise operations.

--------------

Interview

‘Sound business plan needed to increase farm profits’

How will the government plan to promote 10,000 new FPOs by 2023-24 tide over the limitations of the existing farm cooperative system? Edited excerpts from our interview with G.R. Chintala, chairperson, NABARD.

How will the new farm laws and FPO guidelines improve the functioning of farm cooperatives?

NABARD is one of the implementing agencies under the Central Sector Scheme (CSS) for the promotion of 10,000 FPOs and will promote around 4,000 FPOs across the country. The programme will be implemented through select Cluster-Based Business Organisation (CBBOs). As an implementing agency of the scheme, the role of NABARD is to select, guide and monitor CBBOs in the promotion of FPOs, channelise the financial and equity support for their management, among other objectives. [We will] take forward the message of recent agri reforms to the FPOs and their members through an active outreach programme, presently being undertaken.

The SFAC and NABARD have differing data on the FPOs. What changes will the new policy introduce by consolidating all data through the National Project Management Agency (NPMA) it has suggested?

Under the new scheme, SFAC will promote FPOs that will be registered under Companies Act while NABARD will promote FPOs both under Companies Act and Cooperative Societies Act. The variation is in the legal structure of the FPOs, which will impinge only on compliance, whereas the activities / functions of FPOs will obviously remain the same. At the national level, the NPMA will be set up to provide overall project guidance, data maintenance through integrated portal and information management and monitoring. The existing data available with NABARD and SFAC will be integrated with [the] new portal to be developed by NPMA.

The new FPOs will be backed till 2023-24 with a budgetary support of Rs 4,496 crore. But the FPOs also need capacity-building support and may need hand-holding for at least five years, experts tell us.

As per the new policy guidelines, in addition to Rs 18 lakh management cost available to FPOs, there is a provision of Rs 25 lakh per FPOs for the CBBOs. This cost covers the training and capacity building and handholding support expected to be provided by CBBO for a period of five years. At the national level, Bankers Institute of Rural Development (BIRD), a training establishment of NABARD (along with LINAC, a training and research institute for cooperatives), has been identified as Nodal Training institute. BIRD will develop a training framework for the entire programme in terms of developing modules, developing content and also delivery of programmes in an online mode or through partner agencies.

What are the challenges faced by organisations that NABARD supports in terms of developing the overall ecosystem? How do you ensure procurement remunerative prices, ease of doing business (including legal compliance)?

The challenges for the development of the overall ecosystem are the lack of professional management, weak internal governance in FPOs, under-capitalisation to take up activities and also absorb credit, inadequate credit linkages, access to market and inadequate access to infrastructure.

The key elements of successful FPO are financial resources and market linkages. Sound business models require to be developed to achieve the objective of increasing the margins for farmers. To enable that, NABARD at ground level, through the network of partners, government departments at district and state level, will facilitate linkages for FPOs with markets.

Also, we will attempt to integrate these FPOs into digital marketing channels such as e-NAM [National Agriculture Market] and NCDEX [National Commodity & Derivatives Exchange]. FPOs will be encouraged to prepare a sound business plan for their business activities. FPOs will mobilise equity support, as well as credit guarantee cover for bank loans.

The government has provided exemption on payment of income tax for five years to those FPOs having turnover below Rs 100 crore. In addition, we are taking up with the government on providing by working on exemption for Minimum Alternate Tax.

As far as legal compliances are concerned, it may be mentioned that the scheme guidelines necessitate the need for five professionals in each CBBO, including those with knowledge of legal compliance. This will help ensure adequate hand-holding support to FPOs.

(Paliath is an analyst with IndiaSpend.)

We welcome feedback. Please write to respond@indiaspend.org. We reserve the right to edit responses for language and grammar.